AI-Taxi App

AI-Taxi App AI-Food App

AI-Food App AI-Property Mgmt App

AI-Property Mgmt App AI-CRM

AI-CRM AI-Fantasy App

AI-Fantasy App

Web Development

Web Development App Development

App Development Business & Startup

Business & Startup Hire Developer

Hire Developer

Digital Marketing

Digital Marketing Lead-generation

Lead-generation Creative Agency

Creative Agency Branding Agency

Branding Agency Augmented Reality

Augmented Reality Virtual Reality

Virtual Reality Internet of Things

Internet of Things Artificial Intelligence

Artificial Intelligence Blockchain

Blockchain Chatbot

Chatbot

The convenience of the digital age comes with a hidden adversary: digital fraud. From online shopping scams to account takeovers, cybercriminals are constantly devising new methods to steal money and data. But fear not, for on the frontlines of this fight stands a powerful ally: Artificial Intelligence (AI).

The Current report reveals that 37% of participants increased their cybersecurity spending to acquire more advanced security software. AI fraud detection stands out as a key development in the fight against digital fraud. Utilizing advanced algorithms, AI systems can quickly sift through massive datasets to identify irregular patterns and anomalies that may indicate fraudulent behavior. This technology betters the detection process but also learns from each interaction, improving its predictive capabilities over Time.

This technology bolsters security measures while reducing financial losses, safeguarding customer trust, and maintaining the integrity of business operations. This article explores the mechanics of AI fraud detection, the benefits and challenges of using it, and best practices for building a strategy that leverages this technology.

What is AI fraud detection

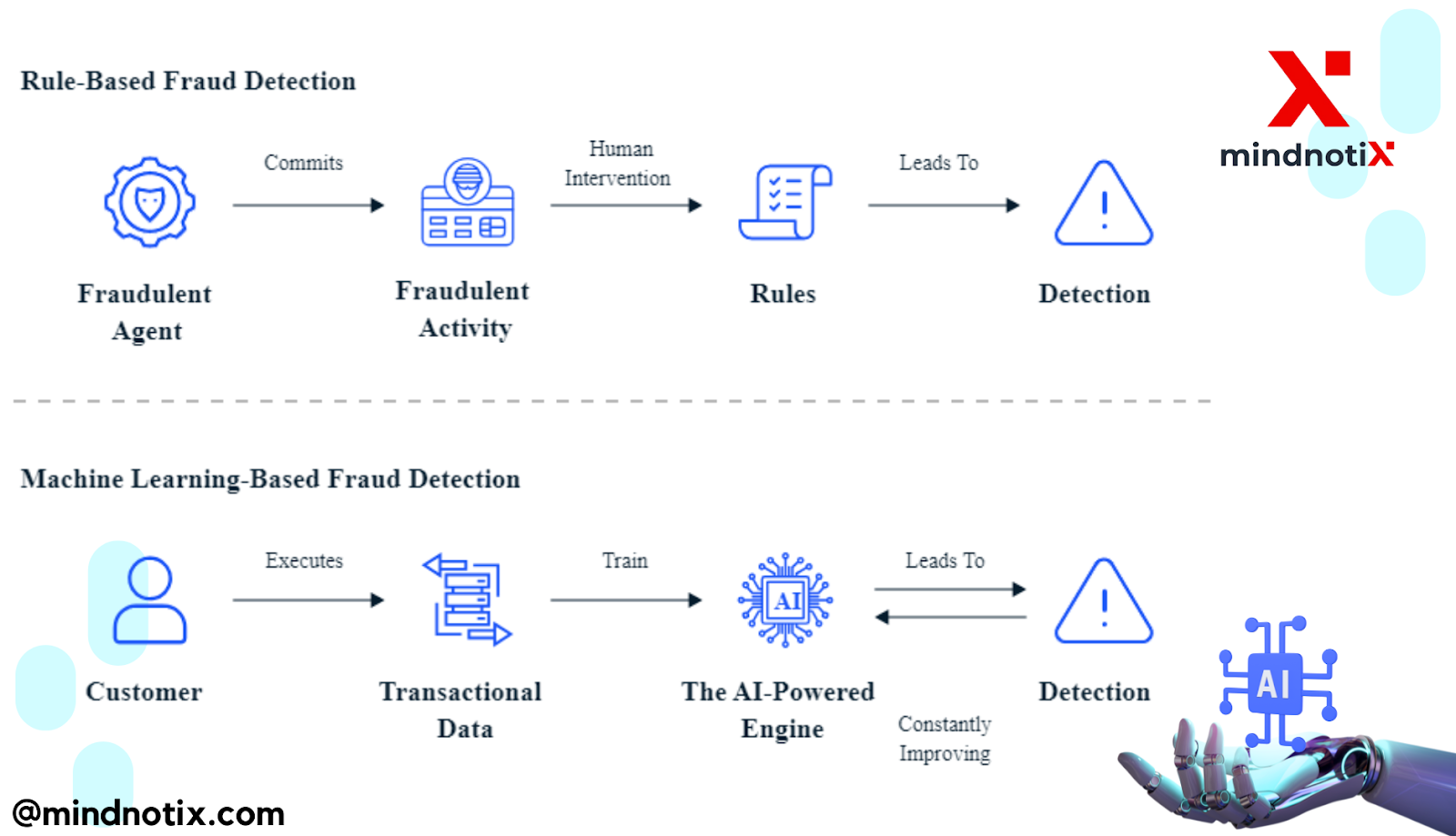

AI fraud detection is a system that uses machine learning to identify fraudulent activity in large datasets. Imagine it as a super-powered security guard that learns from experience. Here's a breakdown of how it works:

Machine learning algorithms analyze vast amounts of data to identify patterns of legitimate transactions and user behavior.

The system is trained to recognize anomalies that deviate from these patterns, which could signal fraud.

As it encounters new data, the AI continuously learns and improves its ability to distinguish real users from fraudsters.

How does AI fraud detection work

AI fraud detection operates by implementing machine learning algorithms that are designed to analyze behaviors and detect anomalies indicative of fraud. It starts by establishing a baseline of normal transaction patterns and user behaviors. The system then continuously monitors data, looking for deviations from this norm. As it encounters new and varied data, the AI model fine-tunes its parameters, differentiating between legitimate and suspicious activities more effectively.

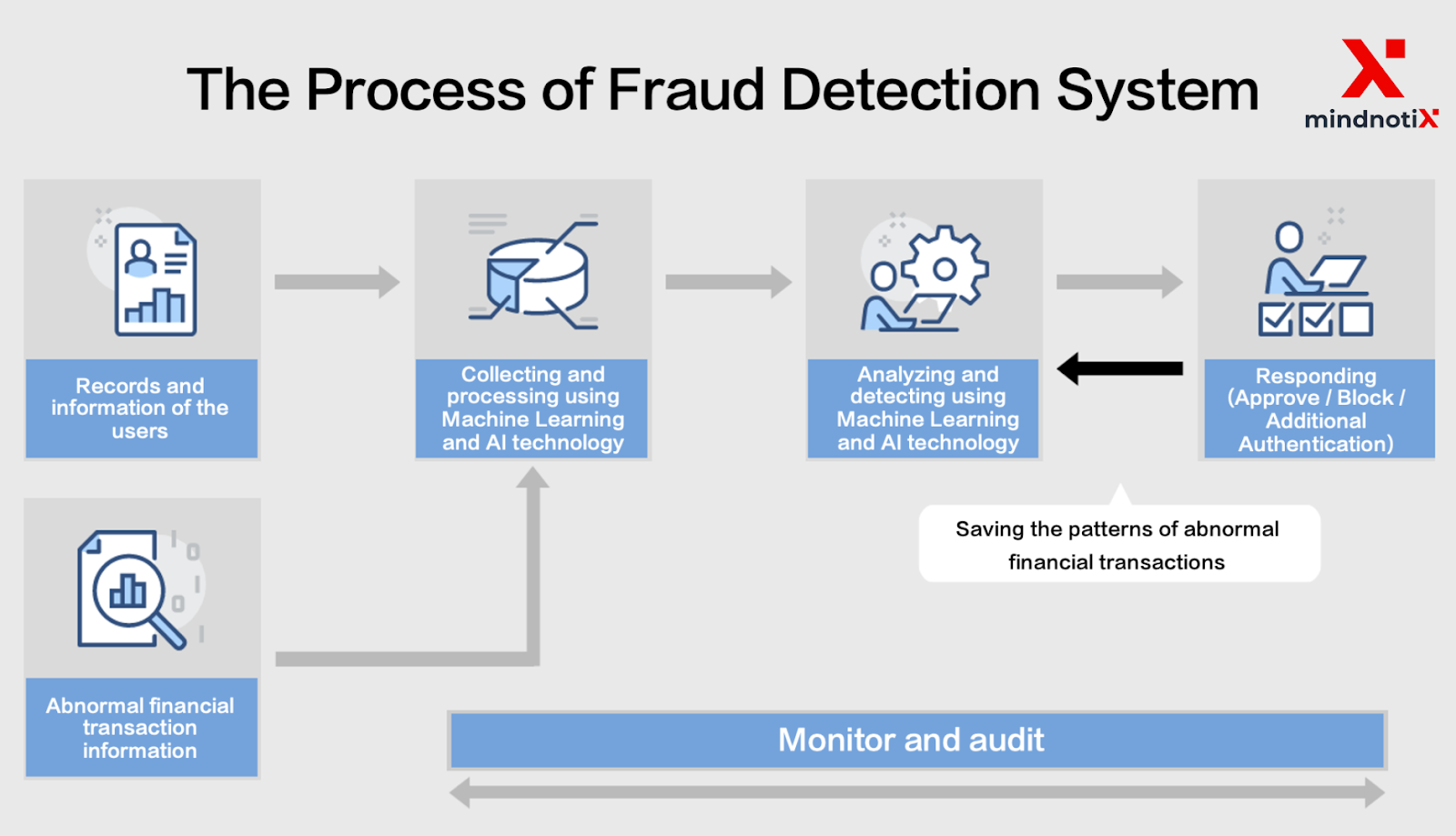

Data Collection: The system gathers information on past transactions, user behavior, and known fraudulent attempts. This data serves as the foundation for learning.

Pattern Recognition: Machine learning algorithms analyze this data to identify patterns in legitimate transactions. These patterns consider factors like purchase history, location, and typical spending amounts.

Anomaly Detection: The system continuously monitors new transactions and user activity. It flags instances that deviate significantly from established patterns, which could indicate potential fraud.

Risk Scoring: AI assigns a risk score to each transaction based on the level of anomaly it detects. Transactions with higher risk scores are flagged for further scrutiny.

Model Refinement: As the system encounters new data, including verified fraudulent attempts, it refines its algorithms to improve accuracy and identify emerging fraud tactics.

AI fraud detection use cases

A report from 2022 suggests that, on average, an organization forfeits 5% of its yearly revenue to fraudulent activities annually, with a median financial impact of $117,000 occurring before the fraud is identified. AI fraud detection is transforming the way industries combat fraud, employing algorithms to spot irregularities and prevent financial losses. Here are a few examples of use cases across industries:

Banking and Finance: AI keeps a watchful eye on accounts, analyzing transaction patterns for suspicious activity. This includes identifying unusual spending habits, large overseas transactions, or attempts to access accounts from unfamiliar locations.

E-commerce: AI helps online retailers combat fraudulent purchases and account takeovers. It can detect suspicious bot activity, flag orders with inconsistencies in billing or shipping addresses, and uncover patterns linked to stolen credit cards.

Insurance: AI can analyze insurance claims to identify fraudulent ones. It can detect patterns in fabricated claims, assess medical records for inconsistencies, and uncover networks of individuals involved in insurance scams.

Telecommunications: AI can thwart fraudulent activities like SIM swapping, where criminals take over phone numbers to access accounts or commit further crimes. It can also identify suspicious call patterns or attempts to bypass network security measures.

Online Gaming: In the world of virtual economies, AI can detect suspicious activity like fake accounts, unauthorized purchases of in-game items, or attempts to manipulate the game for unfair advantage.

The Future of AI fraud detection

AI fraud detection systems offer a range of advantages for businesses looking to safeguard their operations from the ever-evolving threats. By harnessing the power of artificial intelligence, companies can improve security, efficiency, and customer service. Here are some advantages:

Real-time detection and prevention

The ability of AI to monitor transactions 24/7 ensures that any suspicious activity is caught as it happens, allowing for immediate action. Speedy detection is critical in stopping fraudsters and minimizing potential losses. The immediacy of AI response provides businesses with a powerful tool to defend against fraud before it impacts their finances.

Scalability

As transaction volumes grow, AI fraud detection systems can expand their monitoring capabilities without the need for proportional increases in staffing. This scalability is essential for businesses experiencing growth, as it allows them to maintain high levels of fraud detection and prevention without significant additional costs. AI systems can also handle the increased complexity that comes with larger datasets, ensuring that businesses remain protected as they evolve.

Cost reduction

Using AI to detect fraud saves money by preventing fraud losses. It also reduces the financial burden on businesses by cutting down on the need for extensive manual review teams. The automation of fraud detection tasks leads to a more resource-efficient operation, freeing up your team to focus on strategic tasks that require human expertise. Over time, the cost savings realized from using AI can be reinvested into other areas of the business—from building out your product roadmap to investing in marketing ideas.

Increased accuracy

AI’s capacity to analyze data with precision surpasses human capabilities, leading to more accurate identification of fraudulent transactions. These systems are less prone to the errors that can occur with manual reviews. AI algorithms also continuously learn and improve from new data, which means that the system becomes increasingly efficient at detecting fraud over time.

Customer trust and satisfaction

When customers feel secure in their transactions, they are more likely to remain loyal to a business. AI fraud detection helps maintain a safe environment for customers, heightening their trust and satisfaction with the company’s services. A reputation for security can become a significant competitive advantage, attracting new customers who prioritize the safety of their personal and financial information.

Building an AI fraud detection strategy

When rolling out an AI fraud detection strategy, it’s important to adopt a methodical approach that maximizes the system’s effectiveness and efficiency. This means navigating through challenges like data quality, integration, and regulatory compliance, while also establishing a strong operational framework for the AI system. Consider these best practices:

Assemble a Cross-Functional Team: Fraud detection requires expertise from various domains - data security, IT, operations, and business analysts. Building a team with diverse perspectives fosters a holistic approach.

Define Your Goals and Needs: What kind of fraud are you most susceptible to? Identify your priorities - is it catching identity theft, preventing unauthorized account access, or stopping fraudulent transactions? Clear goals will guide your AI model development.

Gather the Right Data: The quality of your data determines the effectiveness of your AI. Collect historical transaction data, user behavior patterns, and verified fraud cases. Ensure data is clean, complete, and up-to-date.

Choose the Right AI Model: Different AI models excel at different tasks. Consider factors like the volume and complexity of your data, the types of fraud you target, and your desired level of real-time detection.

Train and Test Your Model: Train your AI model on your historical data, helping it learn to recognize normal activity and flag anomalies. Rigorously test the model on unseen data to assess its accuracy and identify potential weaknesses.

Continuous Monitoring and Improvement: Fraudsters are like chameleons, constantly changing tactics. Monitor your AI system's performance, refine your models with new data (including recently identified fraud attempts), and stay updated on evolving fraud trends.

Address Ethical Considerations: AI can be a powerful tool, but ethical considerations are crucial. Ensure your data collection practices are transparent and compliant with regulations. Explain how your AI system uses data and prioritize user privacy.

AI Is Predicting The Future Of Online Fraud Detection

Combining supervised and unsupervised machine learning as part of a broader Artificial Intelligence (AI) fraud detection strategy enables digital businesses to quickly and accurately detect automated and increasingly complex fraud attempts.

CONCLUSION :

In conclusion, AI-powered fraud detection has emerged as a game-changer in loss prevention. By leveraging advanced analytics and machine learning, it surpasses traditional methods, offering superior accuracy, adaptability, and efficiency. This translates to significant benefits for businesses, including reduced financial losses, a stronger security posture, and a more streamlined fraud investigation process. As AI technology continues to evolve, its role in safeguarding against financial crime will only become more prominent. However, to fully harness this power, businesses must invest in building a well-defined AI fraud detection strategy, prioritizing data quality, ethical considerations, and continuous improvement. By doing so, they can create a robust shield against evolving fraud threats, fostering trust and confidence with their customers.

For more information contact : support@mindnotix.com

Mindnotix Software Development Company